Exhibit 99.1

SUMMARY

The Combination of TopBuild and USI

We

are the leading purchaser, installer and distributor of insulation products to the United States construction industry based on revenue, with over 250 locations across 46 states. Our installation segment, TruTeam, is a leading provider of insulation

installation services. TruTeam handles every stage of the insulation process, including material procurement, project scheduling and logistics, multi-phase professional installation and installation quality assurance. Our distribution segment,

Service Partners, is a leading distributor of residential fiberglass insulation and insulation related products in the United States. We believe we have a leading national position within the insulation and distribution industries, as our footprint

currently covers 95% of all housing starts and places us in 99 of the top 100 metropolitan statistical areas, or MSAs, in the United States. For the twelve months ended December 31, 2017, we generated net sales and Adjusted EBITDA of

$1,906 million and $198 million, respectively.

On March 1, 2018, we entered into an Agreement and Plan of Merger to

acquire USI (excluding the construction services business) in an all-cash transaction valued at $475 million on a cash-free, debt-free basis. USI is a leading provider of insulation installation and

distribution services to the residential and commercial construction markets. USI has a diversified product and service offering, including fiberglass, spray foam and window and glass installation. USI has 38 locations in 13 states, including high

growth regions in the Pacific Northwest, Mountain West, Southwest and Southeast.

The USI Acquisition demonstrates the continued

successful execution of our business strategy. We believe the USI Acquisition will strengthen our position as the domestic leader in insulation installation and distribution by enhancing our scale, increasing our customer base, strengthening our

position in the supply chain, and diversifying our product offerings. For the twelve months ended December 31, 2017, on a pro forma basis after giving effect to the USI Acquisition, we would have generated combined net sales of

$2,268 million and pro forma Adjusted EBITDA of $259 million, including $15 million of expected synergies.

Combination Rationale

We believe that, following the USI Acquisition, our scale, geographic scope, and product diversification will be significantly

enhanced. The combined company will have a market-leading national installation and distribution platform positioned to deliver the best service to our customers. With significant operational alignment, and comparable

go-to-market strategies, we believe that the USI Acquisition also provides important synergy opportunities, which we expect to execute on within two years post-closing.

Strengthens TopBuild’s position as the leader in the insulation installation and distribution markets

We believe that we will be a market leader in the insulation installation and distribution markets. On a pro forma basis after giving effect

to the USI Acquisition, net sales for the twelve months ended December 31, 2017 would have been $2,268 million, with exposure to regions with more than 95% of residential housing starts

1

across 46 states. We believe that our expansive pro forma footprint will allow us to be the first choice for the industry’s leading homebuilders, and our ability to both install and

distribute allows us to provide value to various customer bases in differing market environments. We see opportunity for the implementation of best practices across the organization that will further enhance our ability to provide well-trained,

experienced operators delivering our value proposition to customers. In a market filled with independent contractors, our respected reputation, strong operating history, and stable, skilled labor force position us to be the first choice for our

customers.

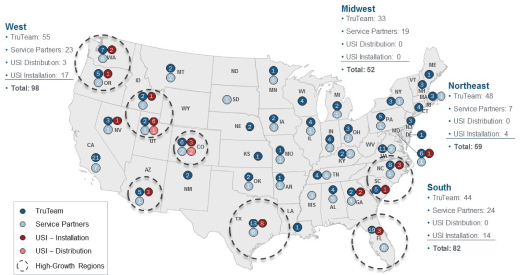

Enhances geographic footprint and penetration in key growth markets

We believe that our expanded and augmented national platform will allow us to better serve our customers. The USI Acquisition broadens our

scale and geographic reach to over 290 facilities across 46 states. While we currently operate in all of the states covered by USI, the acquisition will increase our exposure to many of the higher-growth regions, including the Pacific Northwest,

Mountain West, Southwest, and Southeast regions of the United States.

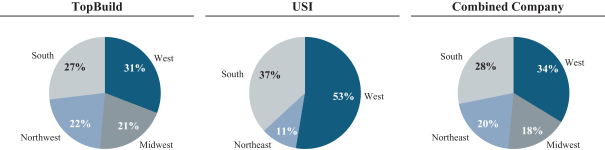

For the twelve months ended December 31, 2017, after giving

pro forma effect to the USI Acquisition, our geographic revenue would have been most exposed to the West region, including high-growth states such as Washington, Oregon, Utah, Colorado and Arizona. The USI Acquisition also increases our exposure to

the South, where USI has operations in North Carolina, South Carolina, Georgia, Florida and Texas.

Net Revenue by Geography for Twelve

Months Ended December 31, 2017

2

Combined National Footprint

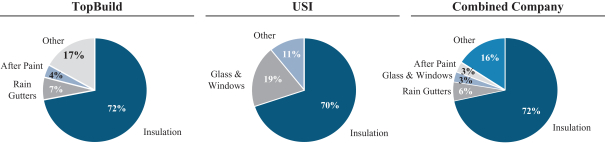

Diversifies business and product mix, enhancing value proposition for customers

We expect that the USI Acquisition will solidify our core insulation business while also expanding our product offerings. We believe that our

increased scale will support our positioning within the insulation value chain, allowing us to provide more attractive solutions to our customers. The acquisition also presents the opportunity to expand our

non-insulation product offerings. Our current offerings include rain gutters, garage doors, fireplaces, fireproofing, shower enclosures and mirrors. The USI Acquisition will expand our offerings to items such

as custom windows and doors and increase our offerings of shower enclosures and mirrors. We believe that we will have significant opportunities to cross-sell these products across our post-acquisition customer base.

Net Sales by End Market Exposure for Twelve Months Ended December 31, 2017

Accretive to TopBuild’s growth and margin profile; robust free cash flow generation supports ability to

deleverage quickly

We believe that the USI Acquisition will be highly complementary with the current financial profile of

TopBuild. For the twelve months ended December 31, 2017, on a pro forma basis after giving effect to the USI Acquisition, including the $15 million of synergies, our Adjusted EBITDA margin would have grown approximately 100 basis points.

On a pro forma basis for 2017, capital expenditures accounted for less than 2 % of revenue, aiding the strong free cash flow generation that has long been a TopBuild hallmark. We plan to continue to focus on driving efficiencies to support our

financial performance.

3

Attractive synergy opportunities within two years of close

We believe the USI Acquisition will result in approximately $15 million of run-rate cost

synergies two years after closing on an annual basis. We expect that these synergies will be realized at both the corporate and branch levels, as well as in our direct materials supply chain.

| |

• |

|

Corporate Synergies: Initiatives include corporate facility rationalization, elimination of redundant professional fees, headcount reductions, and other SG&A-level

costs, such as travel and entertainment. |

| |

• |

|

Branch Level Savings: primarily coming from location rationalization across at least 15 MSAs. We also see opportunities for savings through fleet reductions, general overhead reductions, and non-direct expenses including labor, business insurance, marketing and licensing costs. |

| |

• |

|

Supply Chain: savings on direct materials such as fiberglass, foam mineral wool, and cellulose. These savings are expected to be driven by our increased scale and buying power relative to USI, allowing us to

apply TopBuild’s historically lower material costs to USI’s supply needs. |

It is expected that synergies will be

phased in over the 24 months following close. We anticipate $5-10 million of savings within one year, with the balance being implemented by the end of year two. We estimate $12 million of one-time

costs in 2018 to achieve these identified synergies.

Optimal use of capital, delivering strong shareholder returns

We believe the synergies expected to be produced in this transaction will help drive returns. The USI Acquisition, we believe, will improve

our ability to consistently generate cash flow by realizing greater supply chain efficiencies and expanding our offerings and national footprint. Among other things, our ability to generate cash allows us to both reduce our debt and position

ourselves for future attractive investments.

TopBuild Overview

TopBuild Corp., headquartered in Daytona Beach, Florida, is the leading purchaser, installer, and distributor of insulation products to the

U.S. construction industry, with leading positions in key metropolitan markets. As of December 31, 2017, we operated over 250 locations across 46 states.

Prior to June 30, 2015, we operated as a subsidiary of Masco Corporation, which trades on the NYSE under the symbol “MAS.” We

were incorporated in Delaware in February 2015 as Masco SpinCo Corp., and we changed our name to TopBuild Corp. on March 20, 2015. On June 30, 2015, we separated from Masco, and on July 1, 2015, we began trading on the NYSE under the

symbol “BLD.”

We operate in two segments: our installation segment, TruTeam, and our distribution segment, Service Partners,

which we believe provides us with several distinct competitive advantages. We believe the combined buying power of our two businesses strengthens our ties to the national manufacturers of insulation and other building products, which helps ensure

that we are buying competitively and can maintain adequate material and supplies at our local branches and distribution centers. In addition, the overall effect drives efficiencies throughout our supply chain. Being a leader in both installation and

distribution allows us to effectively reach a broader set of builder customers, regardless of their size or geographic location in the United States.

Our installation segment, TruTeam, has over 175 installation branches located in 41 states across the nation. TruTeam handles every stage of

the insulation process, including material procurement, project

4

scheduling and logistics, multi-phase professional installation, and installation quality assurance. In addition to insulation products, we also install other building products including rain

gutters, fireproofing, garage doors, fireplaces, shower enclosures, and closet shelving. We also offer several services and tools designed to assist builders with applying principles of building science to new home construction through our Home

Services subsidiary and our Environments for Living® program. We believe that our diversified product offerings along with our relationships with contactors are key competitive advantages.

Our distribution segment, Service Partners, has over 70 distribution centers in 32 states across the nation. We distribute insulation and

other building products, including rain gutters, fireplaces, closet shelving, and roofing materials. We believe that our key differentiators are our national scale, stocking of recognized brands along with offering our customers less-than-truckload

(“LTL”) shipments, and same-day and next-day service.

Both our installation (64% of 2017 total sales) and distribution (36% of 2017 total sales) segments maintain a significantly diversified

customer base within the Residential3 (80% of 2017 total sales) and Commercial (20% of 2017 total sales) markets. Our TruTeam segment serves custom builders (34% of 2017 sales), national builders

(33% of 2017 sales), regional builders (20% of 2017 sales), and multi-family builders (12% of 2017 sales). Our business structure allows us to build customer relationships from the ground up. We rely heavily on our local branches to cultivate

builder relationships, regardless of their company size. Concurrently, our regional and national team members develop and sustain relationships with the larger builders to better serve them across their platforms. Our multi-faceted approach allows

us to engage and retain builders of all types. Our Service Partners segment has a customer base consisting of thousands of insulation contractors of all sizes, gutter contractors, weatherization contractors, other contractors, dealers, metal

building erectors, and modular home builders. We believe this diverse customer base reduces the impact of the inherent cyclicality in the homebuilding industry.

Our role in the market as one of the largest single purchasers of insulation has helped us maintain strong relationships with manufacturers of

insulation and other building product suppliers. This positioning helps ensure that we can purchase products at competitive prices, supply our local branches and distribution centers, and drive efficiencies throughout our supply chain.

Major Customers

We have a

diversified portfolio of customers, and no single customer accounted for 3% or more of our total sales for the twelve months ended December 31, 2017. Our top ten customers accounted for approximately 10% of our total sales in 2017. The USI

Acquisition will not only expand our customer base, but we believe that it will also increase our exposure to custom homebuilders, with whom USI has long-standing relationships and high estimated wallet share.

Suppliers

Our businesses depend

on our ability to obtain an adequate supply of high quality products and components from manufacturers and other suppliers. We rely heavily on third party suppliers for our products and key components. We source the majority of our building products

from four primary U.S.-based residential fiberglass insulation manufacturers: Knauf; CertainTeed; Johns Manville; and Owens Corning. Failure by our suppliers to provide us with an adequate supply of high quality products on commercially reasonable

terms, or to comply with applicable legal requirements, could have a material adverse effect on our financial condition and operating results. We believe we currently have positive relationships with our suppliers.

| 3 |

Includes repair and remodel end market. |

5

Employees

At December 31, 2017, we had approximately 8,400 employees. Approximately 700 of our employees are currently covered by collective

bargaining or similar labor agreements. The USI Acquisition will expand our labor headcount by more than 1,800 persons to over 10,200 employees.

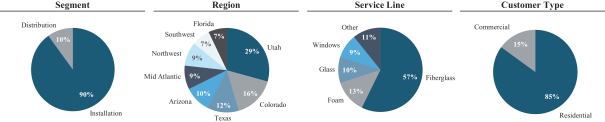

USI

Overview

USI, headquartered in St. Paul, Minnesota, is a leading provider of insulation installation and distribution services to the

residential and commercial construction markets. USI (specifically, United Subcontractors, Inc.) was formed in 1998 and has grown both organically and through acquisitions over the years. Recent acquisitions include Cardalls Insulation (2015), Smith

Insulation (2015), Silver State Specialties (2015), IDS Specialty Building Products (2016), Southern Foam & Coatings (2016), Diamond Glass and Mirror (2017) and Glasshouse (2018). These acquisitions helped drive USI’s continued

expansion across its geographical end markets, as well as continue to diversify its product offerings beyond traditional insulation services. Like TopBuild, USI operates in two segments: installation (90% of 2017 sales) and distribution (10% of 2017

sales). USI has a wide range of product offerings, including various fiber and foam insulation products, residential and commercial windows & glass products, as well as custom closets & shelving, residential garage doors, gutters,

and fireproofing & firestop. Currently, USI has over 1,800 employees at 38 locations in 13 states with significant presence in high-growth markets.

USI’s operations span 13 states and are located in high-growth states in the western and southern United States. Core markets for USI

include western states such as Colorado, Arizona, Utah, Washington and Oregon. Meanwhile, in the South, USI has a strong footprint in states including North Carolina, South Carolina, Georgia, Florida and Texas.

USI Net Sales for Twelve Months Ended December 31, 2017

Industry Overview

The national insulation market was estimated by Grand View Research to be approximately $13.6 billion in 2017 and expected to grow to

approximately $26.7 billion by 2025, at a CAGR of 8.8%. We participate in the residential new build and repair and remodel market, as well as the commercial market.

Insulation continues to play a vital role in the construction practice as the construction industry is trending towards more energy efficient,

sustainable designs. Production of fiberglass insulation products is largely confined to four primary U.S.-based residential fiberglass insulation manufacturers: Knauf; Owens Corning; Johns Manville; and CertainTeed. Insulation installers and

distributors play a pivotal role in the distribution of these manufacturers’ products. Installation and distribution companies provide a consistent, sizable source of demand, reducing the volatility of demand (and production) for manufacturers,

which generally allows the manufacturing process to continue uninterrupted, therefore reducing costly downtime. From the

6

construction standpoint, insulation installation is a pivotal point in the building process because it acts as a gateway for numerous processes to commence, such as Drywall, underlayment,

electrical, HVAC and interior design. Given the tight timelines of construction, a readily available supply of labor becomes imperative in maintaining the timeline, especially as residential construction timelines contract. Employment in the

construction sector was severely reduced during the recession and total employment in the sector remains below peak levels. The ability to retain and supply labor will continue to be an important focus point for installers and contractors alike.

In general, the insulation installation and distribution market’s growth is influenced by general economic cycles, as well as other

factors ranging from socioeconomic, demographic, and lifestyle changes to housing start projections. The shift to urban living that has given rise to multi-family housing starts, which use less insulation per unit, is now being countered by a

resurgence in single-family housing starts in recent years, with strong growth anticipated for 2018. We believe that an overall lack of housing supply along with the increasing age of the U.S. housing stock, currently with a median age of 37 years,

will provide support for growth in housing starts. In the coming years, we expect single-family construction growth to outperform the multi-family space.

Within the insulation market, changes in building codes coupled with evolving environmental and social dynamics have helped elevate the

importance of insulation. From an environmental sustainability standpoint, more insulation results in reduced energy consumption and lower electricity bills. The International Energy Conservation Code (“IECC”) 2012 and 2015 reports

proposed substantial increases in insulation density, which numerous states have adopted in their building codes. IECC resolutions have led to a reduction of energy use intensity of over 40% since the 1970s, with the bulk of the progress seen in the

2009, 2012, and 2015 IECC resolutions. Social, environmental, and economic rationale will continue to determine the development of stricter building codes and could favorably impact the insulation industry.

As a result of stricter building codes shifting consumer preferences, and product innovation, the spray foam insulation market has grown over

the past five years. By creating an air-tight, water resistant seal and offering superior insulating properties, spray foam helps builders adhere to stricter building codes and saves on energy costs. Whereas

spray foam was traditionally used only in custom, high-end homes due to price, the added cost over fiberglass has narrowed, paving the way for the product to be affordable for a larger portion of the market.

The insulation installation and distribution market is highly fragmented with independent regional and local insulation contractors that

are generally family-owned with annual sales of less than $10 million. We believe industry consolidation is driving further supply chain efficiencies and allows for more leveraging of best practices in an effort to deliver a consistent, best-in-class service.

7

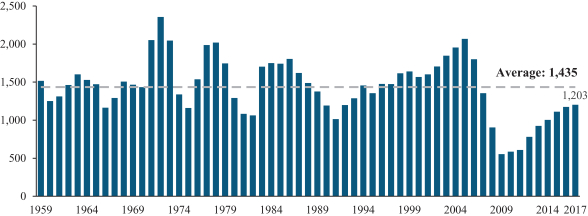

U.S. New Housing Starts (thousands)

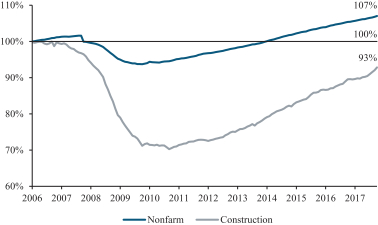

U.S. Monthly Employment (Nonfarm vs. Construction) as Percent of Peak

Competitive Strengths

The market for the distribution and installation of building products is highly fragmented and competitive. Barriers to entry for local

competitors are relatively low, increasing the risk that additional competitors will emerge. Our ability to maintain our competitive position within our industry depends on a number of factors including our national scale, sales channels,

diversified product lines, strong local presence, and strong cash flows.

National scale. With our national footprint, we

provide products and services at all stages of the construction process within the United States. Our national scale, together with our centralized executive management team, allow us to compete locally by:

| |

• |

|

Providing national and regional builders with broad geographic reach, while maintaining consistent policies and practices that enable reliable, high-quality products and services across many geographies and building

sites; |

| |

• |

|

Establishing strong ties to major manufacturers of insulation and other building products, which helps ensure that we buy competitively, maintain availability of supply to our local branches and distribution centers,

and drive efficiencies throughout our supply chain; |

8

| |

• |

|

Providing consistent, customized support and geographic coverage to our customers; |

| |

• |

|

Maintaining an operating capacity that allows us to ramp-up rapidly, without major incremental investment, to target forecasted growth in housing starts and construction activity in each of our lines of business

anywhere in the United States; and |

| |

• |

|

Leveraging investments in systems and processes and sharing best practices across both our installation and distribution segments. |

Two avenues to reach the builder. We believe that having both an installation and distribution business provides a number of

advantages to reach our customers and drive share gains. Our installation business customer base includes builders of all sizes. Our branches go to market with the local brands that small builders recognize and value, and we believe that our

national footprint is appealing to large builders who value consistency across a broad geography. Our distribution business focuses on selling to small contractors who are particularly adept at cultivating local relationships with small custom

builders. Being a leader in both installation and distribution allows us to more effectively reach a broader set of builder customers, regardless of their size or geographic location within the United States, as well as leverage housing growth

wherever it occurs.

Diversified lines of business. In response to the housing downturn in prior years, we enhanced our

ability to serve the commercial construction market. Although the commercial construction market is affected by many of the same macroeconomic and local economic factors that drive residential new construction, commercial construction has

historically followed different cycles than residential new construction. We believe that we have therefore positioned our business to benefit from a greater mix of commercial construction activity than we have historically, which we expect will

help reduce volatility due to reduced dependence on residential new construction while enabling us to better respond to changes in customer demand.

Strong local presence. Competition for the installation and sale of insulation and other building products to builders occurs in

localized geographic markets throughout the country. Builders in each local market have different choices among insulation installers and distributors for their projects, and most builders generally value local relationships, quality, and

timeliness. Our installation branches are locally-branded businesses that are recognized within the communities in which they operate. Our distribution centers service primarily local contractors, lumberyards, retail stores and others who, in turn,

service local homebuilders and other customers. Our operating model, in which individual branches and distribution centers maintain local customer relationships, enables us to develop local, long-tenured relationships with these customers, build

local reputations for quality, service and timeliness, and provide specialized products and personalized services tailored to a geographic region. At the same time, our local operations benefit from centralized functions such as information

technology, credit and purchasing, and the resources and scale efficiencies of an installation and distribution business that has a presence across the United States.

Reduced exposure to residential housing cyclicality. During industry downturns many insulation contractors, who typically buy

directly from manufacturers during industry peaks, return to purchasing through distributors for small, LTL shipments, reducing warehousing needs, and requiring access to purchases on credit. We believe that this drives incremental customers to

Service Partners during these downturns in the business cycle, offsetting decreases at TruTeam as a result of a downturn. Our leadership position in both installation and distribution helps to reduce exposure to cyclical swings in our lines of

business.

Strong cash flow, low capital investment, and favorable working capital fund organic growth. Over the last

several years, we have reduced fixed costs and improved our labor utilization. As a result, we can achieve profitability at lower levels of demand as compared to historical periods. For further discussion on our cash flows and liquidity, see

“Management’s Discussion and Analysis of Financial Condition and Results of Operations of TopBuild Corp.—Liquidity and Capital Resources”.

9

Business Strategy

Maximizing opportunities related to favorable macro drivers. We believe that we are well positioned to capitalize on the

positive macro trends in both the residential and commercial markets. While still a tight labor market, construction hiring has improved in recent years with increased activity, as has commercial and residential construction spending. Housing starts

have recovered significantly since the downturn; however, current starts remain below the 20-year average, indicating there is still opportunity for significant growth. The U.S. Bureau of Census expects

housing starts to grow between 8% and 10% in 2018, and the national ratio of jobs creation to single family home construction is nearly double the long-term average. Commercial starts have grown at double digit rates in recent years and are expected

to continue to grow at this rate in the near term.

Leverage national scale to increase market share organically and through

acquisitions. Between TruTeam and Service Partners, we have the largest network of branches in the United States, with 290+ pro forma locations servicing over 50,000 builders of all sizes nationwide. This scale, paired with our unique

operating model, gives us an advantage with smaller, local builders. Additionally, our localized presence helps us cultivate strong customer relationships and brand loyalty that enhances customer acquisition. We continue to make accretive and

strategic acquisitions a top priority. We look for targets that are complementary to our existing footprint, particularly in high growth regions, that augment our business product mix and capabilities, have a sustainable customer base, and provide

experienced entrepreneurial leaders. We successfully integrated six acquisitions in 2017, and we have completed two acquisitions to date in 2018. These deals were primarily self-sourced and generated through a local pipeline that remains robust.

Drive operational excellence throughout our company to expand margins. Exceptional labor and sales productivity within

TruTeam and seamless supply chain management within Service Partners are key drivers of our margin expansion. Operational efficiency in both segments optimizes our footprint starts and allows us to grow profitably. To adapt to market conditions, we

have added and consolidated branches, cut back on redundancies in work efforts, and concentrated workforces in areas of high demand. While we have executed upon operational initiatives in recent years, we believe that the USI Acquisition presents

new opportunities. We have currently identified $15 million of cost savings that we expect to realize within two years post-closing, and we expect that there is the opportunity to capture more. These synergies are driven by the significant

operational overlap between the two companies, as well as our ability to assume many of USI’s corporate-level responsibilities.

Combine our local relationships with our national resources. TruTeam and Service Partners each have a national reach across all

major MSAs but operate with a local focus. With our national resources, we can offer superior supply chain efficiencies to suppliers in exchange for volume discounts, as well as service national builders across multiple geographies. Simultaneously,

in both segments we exhibit localized knowledge, and we believe that we have optimal service capability and a reputable and well-known brand. The combination of our strong local relationships and national scale has led to the diversification of our

earnings base, as we service a full spectrum of customers and provide supply chain efficiencies to manufacturers of insulation and other products.

Continue product, end market and geographical diversification to mitigate cyclicality. While our core business is insulation, we

offer an extensive array of related products to help service customers of all sizes and needs. We have an established and visible presence across 46 states with many deep-rooted and strong customer relationships with builders of all sizes. The

geographic diversity in these relationships hedges against the potential impacts of losing customers during a cyclical downturn. In addition, during industry downturns, many insulation contractors who typically buy directly from manufacturers during

industry peaks return to purchasing through distributors for small, LTL shipments, reducing warehousing needs and requiring access to purchases on credit. Our ability to service these orders helped shield us from some of the impacts of the most

recent economic

10

downturn. To continue to help mitigate cyclicality, we have increased our exposure to the commercial end-market from 9% in 2005 to 30% in 2017, and we plan

to continue to diversify our end-market exposure in favor of the commercial market. The commercial market offers access to new customers and follows a different operating cycle than the residential market.

11

Summary Historical and Unaudited Pro Forma Financial Data of TopBuild Corp.

The following table presents summary historical and unaudited pro forma condensed consolidated financial data for the Company and its

subsidiaries. The historical financial data for the years ended December 31, 2015, December 31, 2016, and December 31, 2017 are derived from the Company’s audited financial statements. As the Transactions are being presented as

if they occurred at the Company’s fiscal year-end, only audited financial information is presented as part of the historical financial data.

The summary historical financial and other data do not reflect the completion of the Transactions or our capital structure following the

completion of the Transactions and are not indicative of results that would have been reported had the Transactions occurred as of the dates indicated. Data as of and for periods ending on December 31, 2017 or any prior date do not necessarily

reflect what our financial condition and results of operations would have been had we operated as a separate, stand-alone entity during such prior periods. This information is only summary and should be read in conjunction with the information

included in the section entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of TopBuild Corp.,” and the Company’s historical financial statements and the

related notes included elsewhere in this exhibit and the Company’s Annual Report on Form 10-K for the year ended December 31, 2017.

The following summary unaudited pro forma condensed consolidated financial information gives effect to the Transactions. The unaudited pro

forma condensed consolidated statement of operations for the period ended December 31, 2017 reflects the Transactions as if they had occurred on January 1, 2017. The unaudited pro forma condensed consolidated balance sheet as of

December 31, 2017 reflects the Transactions as if they had occurred on December 31, 2017. The pro forma adjustments are based on the information available at the time of the preparation of this exhibit.

The summary unaudited pro forma condensed consolidated financial information that follows is presented for informational purposes only and is

not intended to represent or be indicative of the consolidated results of operations or financial position that would have been reported had the Transactions been completed as of January 1, 2017 (with respect to the statement of operations

data), or as of December 31, 2017 (with respect to balance sheet data), and should not be taken as representative of our future consolidated results of operations or financial position had the Transactions occurred as of such dates. In

connection with the summary unaudited pro forma condensed consolidated financial information, we allocated the preliminary purchase price for the USI Acquisition to the acquired assets and liabilities based upon their estimated fair value. These

estimates are based on financial information available at the time of the preparation of this exhibit. Based on the timing of the closing of the Transactions and other factors, we cannot assure you that the actual adjustments will not differ

materially from the pro forma adjustments reflected in the summary unaudited pro forma combined financial information. It is expected that, following the consummation of the Transactions, we will incur

non-recurring expenses associated with the Transactions and integration of the operations of the two companies. These expenses and integration costs are not reflected in this summary unaudited pro forma

condensed consolidated financial information. Except where specified below, the summary unaudited pro forma condensed consolidated financial information also does not give effect to the potential impact of any anticipated synergies, operating

efficiencies or cost savings that may result from the Transactions.

12

Historical and Unaudited Pro Forma Statement of Operations Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (dollars in thousands) |

|

Year ended

December 31,

2015 |

|

|

Year ended

December 31,

2016 |

|

|

Year ended

December 31,

2017 |

|

|

Year ended

December 31,

2017 |

|

| |

|

|

|

|

|

|

|

|

|

|

Unaudited

Pro Forma |

|

| Statement of Operations Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net sales |

|

$ |

1,616,580 |

|

|

$ |

1,742,850 |

|

|

$ |

1,906,266 |

|

|

$ |

2,267,942 |

|

| Cost of sales |

|

|

1,258,551 |

|

|

|

1,342,506 |

|

|

|

1,445,157 |

|

|

|

1,710,697 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

|

358,029 |

|

|

|

400,344 |

|

|

|

461,109 |

|

|

|

557,245 |

|

|

|

|

|

|

| Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Selling, general and administrative |

|

|

274,498 |

|

|

|

278,740 |

|

|

|

294,245 |

|

|

|

378,274 |

|

| Significant legal settlement |

|

|

— |

|

|

|

— |

|

|

|

30,000 |

|

|

|

30,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total operating expenses |

|

|

274,498 |

|

|

|

278,740 |

|

|

|

324,245 |

|

|

|

408,274 |

|

| Operating income |

|

|

83,531 |

|

|

|

121,604 |

|

|

|

136,864 |

|

|

|

148,971 |

|

| Other income (expense) net: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense: |

|

|

(9,465 |

) |

|

|

(5,608 |

) |

|

|

(8,019 |

) |

|

|

(30,942 |

) |

| Loss on extinguishment of debt |

|

|

— |

|

|

|

— |

|

|

|

(1,086 |

) |

|

|

(1,086 |

) |

| Other, net |

|

|

49 |

|

|

|

277 |

|

|

|

281 |

|

|

|

249 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other expense (net) |

|

|

(9,416 |

) |

|

|

(5,331 |

) |

|

|

(8,824 |

) |

|

|

(31,779 |

) |

| Income before provision for income taxes |

|

|

74,115 |

|

|

|

116,273 |

|

|

|

128,040 |

|

|

|

117,191 |

|

| Provision for income taxes |

|

|

5,008 |

|

|

|

(43,667 |

) |

|

|

30,093 |

|

|

|

45,004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income attributable to continuing operations |

|

$ |

79,123 |

|

|

$ |

72,606 |

|

|

$ |

158,133 |

|

|

$ |

162,195 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loss from discontinued operations, net |

|

$ |

(152 |

) |

|

$ |

— |

|

|

$ |

— |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

78,971 |

|

|

$ |

72,606 |

|

|

$ |

158,133 |

|

|

$ |

162,195 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Historical and Unaudited Pro Forma Balance Sheet Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

| (dollars in thousands) |

|

Year ended

December 31,

2016 |

|

|

Year ended

December 31,

2017 |

|

|

Year ended

December 31,

2017 |

|

| |

|

|

|

|

|

|

|

Unaudited Pro

Forma |

|

| Balance Sheet Data (at end of period): |

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

134,375 |

|

|

$ |

56,521 |

|

|

$ |

38,551 |

|

| Property and equipment, net |

|

|

92,760 |

|

|

|

107,121 |

|

|

|

139,569 |

|

| Total assets |

|

|

1,690,119 |

|

|

|

1,749,549 |

|

|

|

2,305,036 |

|

| Total liabilities |

|

|

717,572 |

|

|

|

753,030 |

|

|

|

1,319,397 |

|

| Equity |

|

|

972,547 |

|

|

|

996,519 |

|

|

|

985,639 |

|

13

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (dollars in thousands) |

|

Year ended

December 31,

2015 |

|

|

Year ended

December 31,

2016 |

|

|

Year ended

December 31,

2017 |

|

|

Year ended

December 31,

2017 |

|

| |

|

|

|

|

|

|

|

|

|

|

Unaudited Pro

Forma |

|

| Other Historical and Unaudited Pro Forma Selected Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| EBITDA(1) |

|

$ |

95,487 |

|

|

$ |

133,615 |

|

|

$ |

152,231 |

|

|

$ |

188,431 |

|

| Adjusted EBITDA(1) |

|

|

107,452 |

|

|

|

144,547 |

|

|

|

197,602 |

|

|

$ |

259,334 |

|

| Adjusted EBITDA Margin(1) |

|

|

6.6 |

% |

|

|

8.3 |

% |

|

|

10.4 |

% |

|

|

11.4 |

% |

| Gross Profit |

|

|

358,029 |

|

|

|

400,344 |

|

|

|

461,109 |

|

|

$ |

557,245 |

|

| Gross Profit Margin |

|

|

22.1 |

% |

|

|

23.0 |

% |

|

|

24.2 |

% |

|

|

24.6 |

% |

| Long-term debt |

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

692,297 |

|

| Long-term debt to Adjusted EBITDA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.7x |

|

| (1) |

In addition to net income determined in accordance with GAAP, we evaluate our operating performance using EBITDA, Adjusted EBITDA, and Adjusted EBITDA Margin. For a description of our use of these non-GAAP financial metrics and their limitations as tools of evaluation, see “Non-GAAP Financial Information.” |

We define EBITDA as net income adjusted for interest expense, net, provision (benefit) for income taxes and depreciation and amortization.

Adjusted EBITDA represents EBITDA as further adjusted for the line items listed in the table below.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (dollars in thousands) |

|

Year ended

December 31,

2015 |

|

|

Year ended

December 31,

2016 |

|

|

Year ended

December 31,

2017 |

|

|

Year ended

December 31,

2017 |

|

| |

|

|

|

|

|

|

|

|

|

|

Unaudited Pro

Forma |

|

| Net income, as reported |

|

$ |

78,971 |

|

|

$ |

72,606 |

|

|

$ |

158,133 |

|

|

$ |

162,195 |

|

| Depreciation & amortization |

|

|

12,108 |

|

|

|

12,011 |

|

|

|

16,453 |

|

|

|

40,578 |

|

| Provision for income taxes |

|

|

(5,008 |

) |

|

|

43,667 |

|

|

|

(30,093 |

) |

|

|

(45,004 |

) |

| Interest expense and other, net |

|

|

9,416 |

|

|

|

5,331 |

|

|

|

7,738 |

|

|

|

30,661 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| EBITDA |

|

|

95,487 |

|

|

|

133,615 |

|

|

|

152,231 |

|

|

|

188,431 |

|

| Share-based compensation(a) |

|

|

4,651 |

|

|

|

7,669 |

|

|

|

9,274 |

|

|

|

9,274 |

|

| Significant legal settlement(b) |

|

|

2,430 |

|

|

|

— |

|

|

|

30,000 |

|

|

|

30,000 |

|

| Rationalization charges(c) |

|

|

4,672 |

|

|

|

3,139 |

|

|

|

3,755 |

|

|

|

3,755 |

|

| Loss on extinguishment of debt(d) |

|

|

— |

|

|

|

— |

|

|

|

1,086 |

|

|

|

1,086 |

|

| Acquisition related costs(e) |

|

|

— |

|

|

|

124 |

|

|

|

1,256 |

|

|

|

3,672 |

|

| Other(f) |

|

|

212 |

|

|

|

— |

|

|

|

— |

|

|

|

4,772 |

|

| Glasshouse(g) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

3,344 |

|

| Estimated Synergies(h) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

15,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Adjusted EBITDA |

|

$ |

107,452 |

|

|

$ |

144,547 |

|

|

$ |

197,602 |

|

|

$ |

259,334 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (a) |

Principally includes stock-based compensation. |

| (b) |

Significant legal settlements occurred in 2015 relating to workers compensation and general insurance claims. A significant legal settlement occurred in 2017 relating to the settlement of a breach of contract action due

to our termination of an insulation supply agreement with Owens Corning. |

| (c) |

Includes compensation associated with eliminated headcount and other restructuring activities. |

| (d) |

A loss on the extinguishment of debt relating to the Credit Agreement. |

14

| (e) |

Costs related to six acquisitions completed in 2017 and one acquisition completed in 2016. In 2017, acquisitions were completed for substantially all the assets of Midwest, EcoFoam, MR Insulfoam, Capital, Superior, and

Canyon. In 2016, the acquisition of substantially all the assets of Valley was completed. |

| (f) |

Consists of estimated results for 2017 with respect to acquisitions by USI, net of results for discontinued operations for 2017. Additionally contains management’s estimated adjustments for 2017 with respect

to expenses not expected to recur in subsequent periods (including, among other things, consulting expenses, board fees, recruiting expenses, transaction expenses and weather-related impacts, including with respect to hurricanes Harvey and Irma).

|

| (g) |

Represents estimated, unaudited results in 2017 for Glasshouse, an entity acquired by USI, prior to its date of acquisition. |

| (h) |

Represents synergies that we expect to realize over time from the acquisition. We will incur significant cash costs in the next twelve months to realize these synergies, and will not fully realize the synergies for

several years. Actual synergies could vary materially from our estimate. |

15

Risks Related to the USI Acquisition

We may not be able to successfully integrate USI and other businesses that we may acquire in the future.

Our ability to successfully implement our business plan and achieve targeted financial results is dependent on our ability to successfully

integrate USI and other businesses that we may acquire in the future. The process of integrating USI, and any other acquired businesses, involves risks. These risks include, but are not limited to:

| |

• |

|

demands on management related to the increase in the size of our business; |

| |

• |

|

diversion of management’s attention from the management of daily operations; |

| |

• |

|

difficulties in the assimilation of different corporate cultures and business practices; |

| |

• |

|

difficulties in conforming the acquired company’s accounting policies to ours; |

| |

• |

|

retaining employees who may be vital to the integration of departments, information technology systems, including accounting systems, technologies, books and records, and procedures, and maintaining uniform standards,

such as internal accounting controls, procedures, and policies; and |

| |

• |

|

costs and expenses associated with any undisclosed or potential liabilities. |

Failure to

successfully integrate USI, or any other acquired businesses, may result in reduced levels of revenue, earnings, or operating efficiency than might have been achieved if we had not acquired such businesses.

In addition, the USI Acquisition will result, and any future acquisitions could result, in the incurrence of additional debt and related

interest expense, contingent liabilities, and amortization expenses related to intangible assets, which could have a material adverse effect on our financial condition, operating results, and cash flow.

We may not be able to achieve the benefits that we expect to realize as a result of the USI Acquisition. Failure to achieve such benefits could have an

adverse effect on our financial condition and results of operations.

We may not be able to realize anticipated cost savings,

revenue enhancements, or other synergies from the USI Acquisition, either in the amount or within the time frame that we expect. In addition, the costs of achieving these benefits may be higher than, and the timing may differ from, what we expect.

Our ability to realize anticipated cost savings, synergies, and revenue enhancements may be affected by a number of factors, including, but not limited to, the following:

| |

• |

|

the use of more cash or other financial resources on integration and implementation activities than we expect; |

16

| |

• |

|

unanticipated increases in expenses unrelated to the USI Acquisition, which may offset the expected cost savings and other synergies from the USI Acquisition; |

| |

• |

|

our ability to eliminate duplicative back office overhead and redundant selling, general, and administrative functions; and |

| |

• |

|

our ability to avoid labor disruptions in connection with the integration of USI, particularly in connection with any headcount reduction. |

Specifically, while we expect the USI Acquisition to create significant opportunities to reduce our combined operating costs, these cost

savings reflect estimates and assumptions made by our management, and it is possible that our actual results will not reflect these estimates and assumptions within our anticipated timeframe or at all.

If we fail to realize anticipated cost savings, synergies, or revenue enhancements, our financial results may be adversely affected, and we

may not generate the cash flow from operations that we anticipate.

USI may have liabilities that are not known to us.

USI may have liabilities that we failed, or were unable, to discover in the course of performing our due diligence investigations of USI. We

cannot assure you that the indemnification available to us under the acquisition agreement in respect of the USI Acquisition or the representation and warranty insurance procured by us in connection with such agreement will be sufficient in amount,

scope or duration to fully offset the possible liabilities associated with USI’s business or property that we will assume upon consummation of the USI Acquisition. We may learn additional information about USI that materially adversely affects

us, such as unknown or contingent liabilities and liabilities related to compliance with applicable laws. Any such liabilities, individually or in the aggregate, could have a material adverse effect on our business, financial condition and results

of operation.

17

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION

The following unaudited pro forma condensed consolidated financial information is based on the historical audited consolidated

financial statements of TopBuild and USI appearing elsewhere in this exhibit and in the Company’s annual report on Form 10-K for the year ended December 31, 2017, as adjusted to illustrate the estimated pro forma effects of the Transactions.

The unaudited pro forma condensed consolidated financial information should be read in conjunction with the consolidated financial statements and related notes of TopBuild and USI and other financial information appearing elsewhere in this exhibit

and in the Company’s annual report on Form 10-K for the year ended December 31, 2017

The unaudited pro forma balance sheet gives

effect to the Transactions as if they had occurred on December 31, 2017. The unaudited pro forma statement of operations give effect to the Transactions as if they had occurred as of January 1, 2017.

The unaudited pro forma adjustments are based upon available information and certain assumptions that we believe are reasonable. The pro forma

adjustments and certain assumptions underlying these adjustments are described in the accompanying notes, which should be read in conjunction with the unaudited pro forma financial information. The pro forma adjustments are included only to the

extent they are (i) directly attributable to the Transactions, (ii) factually supportable and (iii) with respect to the pro forma statements of operations, expected to have a continuing impact on results. In addition, the unaudited

pro forma financial information has been compiled in accordance with the accounting policies of TopBuild as set out in the historical financial statements of TopBuild included in TopBuild’s annual report on Form 10-K for the year ended December

31, 2017.

Our acquisition of USI will be accounted for and is presented in the unaudited pro forma condensed consolidation financial

information as a purchase business combination in accordance with Accounting Standards Codification (“ASC”) 805, Business Combinations. Under ASC 805, the excess of the purchase price over the fair value of net assets acquired and

liabilities assumed is recorded as goodwill. The pro forma adjustments reflect our preliminary estimates of the purchase price allocation related to our acquisition of USI. However, as of the date of this exhibit, we have not performed the valuation

studies necessary to determine with any certainty the fair values of the assets that we will acquire and the liabilities that we will assume and the related allocation of purchase price. The purchase price allocation is subject to change based upon

finalization of appraisals and other valuation studies that we will arrange to obtain, and the amounts contained in the final purchase price allocation may differ materially from our preliminary estimates. For purposes of computing pro forma

adjustments, we have assumed that historical values of assets acquired and liabilities assumed reflect fair value. The pro forma balance sheet includes a preliminary estimate of fair value adjustments for property and equipment and identifiable

intangible assets such as tradenames and customer contracts, and the pro forma condensed consolidated statements of operations includes preliminary estimates of incremental depreciation and amortization expenses associated with the above described

fair value adjustments. However, these amounts are subject to change as we have not completed the appraisal process as of the date of this exhibit. The pro forma adjustments do not include adjustments to deferred tax assets or liabilities other than

with respect to USI’s historical goodwill and our preliminary estimate of the purchase price to be allocated to property and equipment and identifiable intangible assets and goodwill.

Revisions to the preliminary purchase price allocation, interest rates and financing costs could materially change the pro forma amounts of

total assets, total liabilities, invested equity, depreciation and amortization, interest expense and income tax expense presented herein. The structure of the Transactions and certain elections that we may make in connection with our acquisition of

USI and subsequent tax filings may impact the amount of deferred tax liabilities that are due and the realization of any deferred tax assets.

The unaudited pro forma condensed consolidated financial information contained in this exhibit is for informational purposes only and is not

intended to represent or be indicative of the consolidated results of operations or financial position that we would have reported had the Transactions been completed as of the dates presented and should not be taken as representative of our future

consolidated results of operations or financial position.

18

Condensed Consolidated Balance Sheet (Unaudited)

(dollars in thousands)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

As of

December 31, 2017 |

|

| |

|

Historical

TopBuild |

|

|

Historical

USI |

|

|

Acquisition

Adjustments

(a) |

|

|

Financing

Adjustments |

|

|

Pro Forma |

|

| ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Current assets: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

56,521 |

|

|

$ |

18,167 |

|

|

$ |

(493,167 |

)(b) |

|

$ |

457,030 |

(b) |

|

$ |

38,551 |

|

| Receivables, net of an allowance for doubtful accounts of $3,673 and $3,374 at December 31,

2017, and December 31, 2016, respectively |

|

|

308,508 |

|

|

|

57,593 |

|

|

|

|

|

|

|

|

|

|

|

366,101 |

|

| Inventories, net |

|

|

131,342 |

|

|

|

15,605 |

|

|

|

|

|

|

|

|

|

|

|

146,947 |

|

| Prepaid expenses and other current assets |

|

|

15,221 |

|

|

|

3,291 |

|

|

|

|

|

|

|

|

|

|

|

18,512 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total current assets |

|

|

511,592 |

|

|

|

94,656 |

|

|

|

(493,167 |

) |

|

|

457,030 |

|

|

|

570,111 |

|

| Property and equipment, net |

|

|

107,121 |

|

|

|

25,243 |

|

|

|

7,205 |

(a) |

|

|

|

|

|

|

139,569 |

|

| Goodwill |

|

|

1,077,186 |

|

|

|

160,623 |

|

|

|

80,391 |

(a) |

|

|

|

|

|

|

1,318,200 |

|

| Other intangible assets, net |

|

|

33,243 |

|

|

|

100,253 |

|

|

|

117,347 |

(a) |

|

|

|

|

|

|

250,843 |

|

| Deferred tax assets, net |

|

|

18,129 |

|

|

|

— |

|

|

|

4,540 |

(a) |

|

|

|

|

|

|

22,669 |

|

| Other assets |

|

|

2,278 |

|

|

|

1,366 |

|

|

|

|

|

|

|

|

|

|

|

3,644 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total assets |

|

$ |

1,749,549 |

|

|

$ |

382,141 |

|

|

$ |

(283,684 |

) |

|

$ |

457,030 |

|

|

$ |

2,305,036 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| LIABILITIES AND EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Current liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Accounts payable |

|

$ |

263,814 |

|

|

|

12,563 |

|

|

$ |

|

|

|

$ |

|

|

|

$ |

276,377 |

|

| Current portion of long-term debt |

|

|

12,500 |

|

|

|

1,200 |

|

|

|

(1,200 |

)(c) |

|

|

5,000 |

(c) |

|

|

17,500 |

|

| Accrued liabilities |

|

|

75,087 |

|

|

|

27,350 |

|

|

|

|

|

|

|

|

|

|

|

102,437 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total current liabilities |

|

|

351,401 |

|

|

|

41,113 |

|

|

|

(1,200 |

) |

|

|

5,000 |

|

|

|

396,314 |

|

| Long-term debt |

|

|

229,387 |

|

|

|

118,294 |

|

|

|

(118,294 |

)(c) |

|

|

462,910 |

(c) |

|

|

692,297 |

|

| Deferred tax liabilities, net |

|

|

132,840 |

|

|

|

20,375 |

|

|

|

38,169 |

(d) |

|

|

|

|

|

|

191,384 |

|

| Long-term portion of insurance reserves |

|

|

36,160 |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

36,160 |

|

| Other liabilities |

|

|

3,242 |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

3,242 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities |

|

|

753,030 |

|

|

|

179,782 |

|

|

|

(81,325 |

) |

|

|

467,910 |

|

|

|

1,319,397 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Commitments and contingencies |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Equity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Preferred stock, $0.01 par value: 10,000,000 shares authorized; 0 shares issued and outstanding at

December 31, 2017, and December 31, 2016 |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

— |

|

| Common stock, $0.01 par value: 250,000,000 shares authorized; 38,626,378 issued and 35,586,916

outstanding at December 31, 2017, and 38,488,825 shares issued and 37,815,199 outstanding at December 31, 2016 |

|

|

386 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

386 |

|

| Treasury stock, 3,039,462 shares at December 31, 2017, and 673,626 shares at December 31,

2016, at cost |

|

|

(141,582 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(141,582 |

) |

| Additional paid-in capital |

|

|

830,600 |

|

|

|

202,359 |

|

|

|

(202,359 |

)(e) |

|

|

|

|

|

|

830,600 |

|

| Retained earnings |

|

|

307,115 |

|

|

|

|

|

|

|

|

|

|

|

(10,880 |

)(a)(h) |

|

|

296,235 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total equity |

|

|

996,519 |

|

|

|

202,359 |

|

|

|

(202,359 |

) |

|

|

(10,880 |

) |

|

|

985,639 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities and equity |

|

$ |

1,749,549 |

|

|

$ |

382,141 |

|

|

$ |

(283,684 |

) |

|

$ |

457,030 |

|

|

$ |

2,305,036 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19

TopBuild Corp.

Condensed Consolidated Statement of Operations (Unaudited)

(in thousands, except common share amounts)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Year Ended

December 31, 2017 |

|

| |

|

Historical

TopBuild |

|

|

Historical

USI |

|

|

Acquisition

Adjustments |

|

|

Financing

Adjustments |

|

|

Pro Forma |

|

| Net sales |

|

$ |

1,906,266 |

|

|

$ |

361,676 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

2,267,942 |

|

| Cost of sales |

|

|

1,445,157 |

|

|

|

271,102 |

|

|

|

(5,562 |

)(f) |

|

|

— |

|

|

|

1,710,697 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

|

461,109 |

|

|

|

90,574 |

|

|

|

5,562 |

|

|

|

— |

|

|

|

557,245 |

|

| Selling, general, and administrative expense (exclusive of significant legal settlement, shown

separately below) |

|

|

294,245 |

|

|

|

77,329 |

|

|

|

6,700 |

(f),(g) |

|

|

— |

|

|

|

378,274 |

|

| Significant legal settlement |

|

|

30,000 |

|

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

30,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating profit |

|

|

136,864 |

|

|

|

13,245 |

|

|

|

(1,138 |

) |

|

|

— |

|

|

|

148,971 |

|

| Other income (expense), net: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest expense |

|

|

(8,019 |

) |

|

|

(11,353 |

) |

|

|

— |

|

|

|

(11,570 |

)(i) |

|

|

(30,942 |

) |

| Loss on extinguishment of debt |

|

|

(1,086 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(1,086 |

) |

| Other, net |

|

|

281 |

|

|

|

(32 |

) |

|

|

— |

|

|

|

— |

|

|

|

249 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other expense, net |

|

|

(8,824 |

) |

|

|

(11,385 |

) |

|

|

— |

|

|

|

(11,570 |

) |

|

|

(31,779 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations before income taxes |

|

|

128,040 |

|

|

|

1,860 |

|

|

|

(1,138 |

) |

|

|

(11,570 |

) |

|

|

117,191 |

|

| Income tax benefit (expense) from continuing operations |

|

|

30,093 |

|

|

|

9,827 |

|

|

|

455 |

(i) |

|

|

4,628 |

(j) |

|

|

45,004 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations |

|

|

158,133 |

|

|

|

11,687 |

|

|

|

(683 |

) |

|

|

(6,942 |

) |

|

|

162,195 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

$ |

158,133 |

|

|

$ |

11,687 |

|

|

$ |

(683 |

) |

|

$ |

(6,942 |

) |

|

$ |

162,195 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income per common share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Weighted average number of common shares outstanding |

|

|

35,897,641 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35,897,641 |

|

| Income from continuing operations |

|

|

4.41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.52 |

|

| Loss from discontinued

operations, net |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

— |

|

| Net income |

|

|

4.41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.52 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|